Fidelity Investments Inc. or also known as Fidelity is a privately-owned investment management company which provides multinational financial services. This company was based in Boston, Massachusetts and established in 1946. Fidelity was named as one of the largest asset managers in the world.

Fidelity now offers a variety of financial services including wealth management, fund distribution and investment advice, retirement services, life insurance, and securities execution and clearance.

One of the promising Fidelity services is Investment Retirement Plan Services. This Fidelity service ensures your saving strategy works as you are. So, do you want to learn about the Fidelity Retirement service through our page? Okay, let’s see our explanation below!

How to View Your Pension Summary on Fidelity?

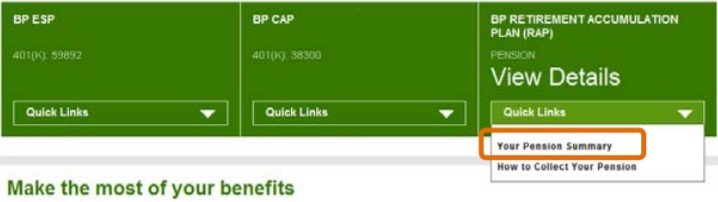

To view your pension summary, you can use ‘Quick Links’. The Quick Link here provides direct access to your pension summary screen and the instructions on how to gather your pension. If you want to access your estimated BP RAP benefit, you have to choose ‘Your Pension Summary’.

Here’s how to access your pension summary!

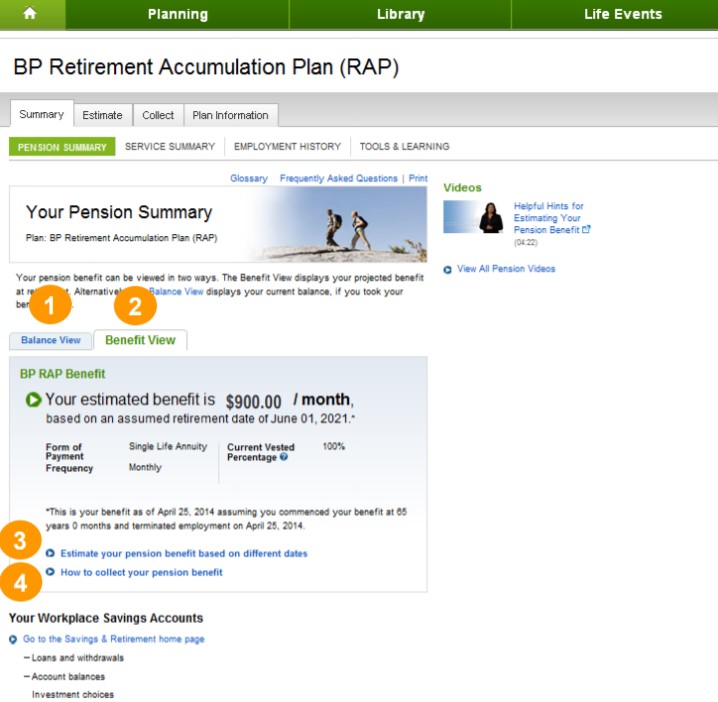

- When you want to view your pension summary, you can go to the ‘Balance View’ section. However, this section will show your total qualified cash balance account. Otherwise, if you do not have a cash balance account, the Balance View is not available.

- If you want to see your estimated benefit per month, you can go to the ‘Benefit View’ section. Your estimated benefit per month here is obtained, assuming you cease working on the current date and your benefit will then begin at age 65.

- If you want to model your benefit based on different termination and commencement dates, you can use the ‘Estimate your pension benefit based on different dates’ link.

- If you want to know step-by-step instructions for initiating your retirement election online, you can click on the ‘How to collect your pension benefit’ link.

Note: You’re able to access the online modeling tool by clicking the Estimate tab located at the top of the screen.

Here’s for Estimate a Pension Benefit Payment!

Fidelity also provides some online benefit modeling tools which can allow you to estimate and compare different payment amounts and schedules which may be available for you. With the use of this tool, you can save snapshots of estimates, compare scenarios, and even initiate your retirement if you’re eligible.

What you can do with modeling different benefit scenarios include:

- Enter the date or age you plan to retire from BP.

- Enter the date or age you plan to begin receiving your pension benefit.

- If applicable, add a beneficiary option.

- Enter interest rate and salary details.

It’s important to note, you can click on the ‘How does this impact my estimate’ for additional information on how the above attributes affect your estimate.

Here’s how to add different scenarios and calculate!

- First option, you can click on the ‘Add another scenario’ section to model different retirement and commencement ages. Then, you’re able to model and compare up to three scenarios and one time.

- Second option, you can click on the ‘Calculate Payment Options’ section to view the benefit estimates for each scenario.

Well, that’s Fidelity guides for pension summary. Moreover, Fidelity NetBenefits will assist you get ready in a quick and easy way. What you need to do is to log on at any time you choose to view and manage your accounts, research the investment options available under Savings plans, access planning tools and resources, as well as view messages from BP related to your benefits and many more.

Fidelity Guidelines for Pension Planning

Fidelity also provides a bunch of guidelines for your pension saving. This guide certainly makes it easy for you to save for retirement and also balance your income for the present. Here, you need to stretch your income and the priorities will make your head spin.

You need to remember that time is such an important key thing in your pension saving. It means that if you choose to save less now, you will have three choices including work longer or spend less in pension, save more later or some combination of them.

Here are Fidelity’s guidelines for your pension saving:

1. Accept the offer of retirement planning from your workplace

If the company you work for offers a retirement plan, accept the offer. You must make this opportunity your priority and your main goal. Make sure to take advantage of the entire game, however basically it’s “free” money.

Generally, companies offering retirement plans will match your contributions dollar-for-dollar or 50 cents, up to a certain percentage of your contribution. What you have to do here is to check if you are currently contributing enough to get this offer matched or not. If not, take a consideration to adjust your contribution amount to get that “free” money.

2. Manage your contributions automatically

Managing up automatic contributions is arguably one of the easiest and most widely used ways to make saving a regular habit. Fidelity also recommends you to manage automatic contributions to your entirement with your paycheck, so you do not need to think about it as well.

In this case, automatic contributions will ensure you prioritize your pension planning and spread investment risk over time.

3. Make sure to save 15% per year

If you can take up the challenge of saving 15% per year of your pretax income for retirement, you’re a pretty great person. This savings includes your contributions to workplace plans and any additional IRAs, aside from the appropriate contributions or employer revenue sharing.

We think that your aim will be successful if you do the following important things:

- Saving consistently

- Get started early

- Invest wisely, much like saving in a tax-advantaged retirement savings account such as 401(k)s, 403(b)s, Health Savings Accounts (HSA), or IRAs.

However, if you have not been able to save the full 15% each year, you don’t have to worry. Alternatively, you can try to make small cuts in your daily expenses or even save an additional 1% more which will have the potential to grow.

AUTHOR BIO

On my daily job, I am a software engineer, programmer & computer technician. My passion is assembling PC hardware, studying Operating System and all things related to computers technology. I also love to make short films for YouTube as a producer. More at about me…

Leave a Reply