Fidelity seems to answer your desire to plan and save your retirement money well and organized. With a variety of Fidelity retirement services, you definitely can make contributions for your pension savings correctly. From now on, make sure to take consideration to make contributions for your pension savings with Fidelity.

As a beginner for your pension savings, you may need some guides which will tell you about the retirement plans, to finally pick the Fidelity retirement service. Thankfully, this post will show you how the Fidelity NetBenefits works for your pension savings. So, if you are interested in choosing the retirement plans with Fidelity, you can read the guides through our post below!

Fidelity Retirement Service Overview

Fidelity offers pension plans through its subsidiary Fidelity Personal, Workplace and Institutional Services (PWIS). As of September 30, 2015, this subsidiary recorded over $1.4 trillion in assets under administration and $32 billion in defined contribution assets.

Aside from pension planning, this subsidiary also offers pension administration, record-keeping services and stock plan administration, as well as health and welfare plan administration.

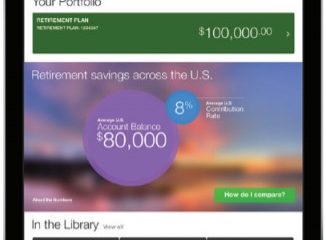

The pension plan services such give you ease of saving that you will allocate for your old age. Of course we already understand that saving for retirement is not instant, and not like a marathon. It is not always easy to know if you are on the right track in saving for your retirement.

With Fidelity Retirement services, they can help you stay on the right track so that your goal of saving for retirement is faster. Fidelity company recommends that you save 15% of your income, if you calculate that you work until you are 67, in this case including employer-matched contributions.

Here’s for the simulation:

- If you are now in your 20s or 30s, Fidelity recommends you to save an amount equal to your salary by age 30. Here, you need to worry if you have not, you just simply get started as soon as you can.

- If you are now in your 40s or early 50s, it’s highly recommended for you to save 3 times your salary by age 40 and 6 times by 50. However, saving is very important as you are closer to the time when you will need more money.

- If you are now less than 15 years from retirement, but you’re still short of your savings goal. Here, you need to try increasing your income percentage that you save, as the finish line is in sight.

Collecting Your Pension, Here’s the Guide!

If you want to collect your pension, you can utilize the ‘Collect’ section. However, this section will provide the information that you will have to initiate your retirement and describes the three-step process which you will follow to collect your pension.

Here’s how to access the ‘Collect’ section!

- Choose the ‘How to Collect’ sub-tab.

- Then, click on ‘Your Profile’ to access and update your profile.

- You can click on the ‘Get Started Now’ to see the ‘Collect Your Pension’ screen.

- It’s important to note, you can also click on the ‘Estimate’ tab to model or edit specific and benefit commencement dates. If needed, you can review additional resources.

- After that, you need to click on the ‘Start Now’ to show the collect your pension screen.

- Then, you can review your personal information and check ‘Agree’ if the information is correct.

- Last, click ‘Next’.

To note, you can click on the ‘Your Profile’ link to update incorrect profile data. In this case, the active employees may have to contact BP directly to update applicable profile information.

Consider for Your Pension Savings with IRA

An IRA or ‘Indivual Retirement Account’ will allow you to save your money for your pension in a tax-advantaged way. You can create an IRA account through a financial institution which allows you to save for retirement with tax-free growth.

Why should you consider the IRA? In fact, there are a lot of financial experts that estimate that you will need up to 85% of your pre-retirement income in retirement. We think that your employer-sponsored retirement savings plan may not be enough to raise the savings you need.

Unfortunately, a Fidelity IRA provides help to add your current savings in your employer-sponsored pension plan. You can also get access to a potentially wider bunch of investment options than your company sponsored plan. With Fidelity IRA, you can take advantage of the potential for tax-deferred or tax-free growth.

You can also try to contribute the maximum amount to your IRA each year in order to gain the most out of these savings. Make sure to observe your investments and make adjustments needed.

There are at least three main types of IRAs where each has different advantages:

Traditional IRA

With this type of IRA, you can make contributions with money that you may deduct on your tax return. Then, any earnings will potentially grow tax-deferred until you withdraw them in retirement. A lot of retirees will find themselves in a lower tax bracket than they were in pre-retirement. Well, the tax-deferral means the money that you may be taxed at a lower rate.

If you’re interested in opening a Traditional IRA, you can register here.

Roth IRA

With this type of IRA, you can make contributions with money that you have already paid taxes on. Your money may potentially then grow tax-free, with tax-free withdrawals in retirement, provided that certain conditions are met.

If you’re interested in opening a Roth IRA, you can register here.

Rollover IRA

With this type of IRA, you can make contributions by donating money ‘rolled over’ from a qualified retirement plan into this traditional IRA. In this case, Rollovers involve transferring of eligible assets from an employer-sponsored plan such as a 403(b), 401 (k), into an IRA.

If you’re interested in opening a Rollover IRA, you can register here.

Whatever the type of IRA you choose, well, the tax benefits will keep allowing your savings to potentially rise or compound, faster than in a taxable account.

AUTHOR BIO

On my daily job, I am a software engineer, programmer & computer technician. My passion is assembling PC hardware, studying Operating System and all things related to computers technology. I also love to make short films for YouTube as a producer. More at about me…

Leave a Reply